Deductible vs. Co-Pay vs. Coinsurance: Breaking Down the Basics of Health Insurance

If you’ve ever handed over your insurance card at a doctor’s office, only to be asked for a small payment say $10, $25, or even $50 you’ve already met one of the key players in health insurance: the co-pay. But co-pays are just one part of the puzzle. To really understand how your health insurance works (and avoid surprise bills), you need to know how deductibles, co-pays, and coinsurance work together.

Let’s break it down in plain English with examples, visuals, and a few tips to help you make smarter choices.

What Is a Co-Pay?

A co-pay is a fixed fee you pay for specific health services. It’s usually due at the time of your appointment or when picking up a prescription. Co-pays are your way of sharing the cost of care with your insurance company.

Common co-pay examples:

- $20 for a primary care visit

- $35 for a specialist

- $10 for generic prescriptions

- $50 for urgent care

Different services have different co-pays, and they’re usually listed in your insurance plan summary. Plans with lower monthly premiums often have higher co-pays, while plans with higher premiums tend to offer lower co-pays.

Tip: If you visit the doctor frequently or take regular medications, a plan with lower co-pays might save you money even if the monthly premium is higher.

What Is a Deductible?

Your deductible is the amount you must pay out-of-pocket before your insurance starts covering costs. Think of it as the “entry fee” to activate your coverage.

Let’s say you have a $2,000 deductible. That means you’ll pay the first $2,000 of your medical bills yourself. After that, your insurance starts helping out either by covering costs fully or splitting them with you through coinsurance.

Example: Jim has a high-deductible plan with a $5,000 deductible. He needs surgery that costs $7,000. Here’s how it breaks down:

- Jim pays the first $5,000 (his deductible).

- The remaining $2,000 is split between Jim and his insurance, depending on his coinsurance rate.

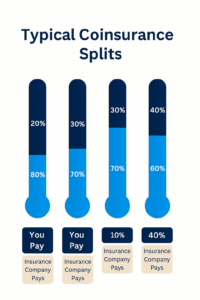

What Is Coinsurance?

Once your deductible is met, coinsurance kicks in. This is a percentage split between you and your insurance company. Unlike co-pays (which are fixed), coinsurance is based on the total cost of care.

Back to Jim’s example:

- His deductible is paid.

- His coinsurance rate is 20%.

- For the remaining $2,000 of his surgery, Jim pays $400 (20%), and his insurance pays $1,600 (80%).

Coinsurance applies to many services, including hospital stays, surgeries, and specialist care. It’s your share of the cost after the deductible is met.

What About Premiums?

Your premium is the monthly fee you pay to keep your insurance active. It’s like a subscription you pay it whether or not you use your insurance that month.

Premiums don’t count toward your deductible or coinsurance, but they’re part of your total cost. Plans with lower premiums often come with higher deductibles and coinsurance rates, while higher-premium plans offer more coverage upfront.

If you want to learn more about “insurance premiums” please check out our last blog regarding this topic.

Out-of-Pocket Maximum: Your Safety Net

Here’s the good news: most insurance plans include an out-of-pocket maximum the cap on what you’ll pay in a year. Once you hit that limit, your insurance covers 100% of eligible costs for the rest of the year.

What counts toward the out-of-pocket max?

- Deductibles

- Coinsurance

- Co-pays

What doesn’t count?

- Monthly premiums

- Non-covered services

- Out-of-network care (in some plans)

Under the Affordable Care Act (ACA), all compliant plans sold through the Health Insurance Marketplace must include an out-of-pocket maximum. In 2025, the legal limit for individual plans is around $9,450, and $18,900 for families.

Plans That Don’t Follow These Rules

Not all plans include deductibles, coinsurance, or out-of-pocket maximums. Some exceptions include:

- Short-term plans: Temporary coverage with limited benefits

- Grandfathered plans: Older plans not updated to ACA standards

- Limited benefit plans: Coverage for specific services only (e.g., accident-only or vision-only)

These plans may have lower premiums but offer less protection. Always read the fine print and ask questions before enrolling.

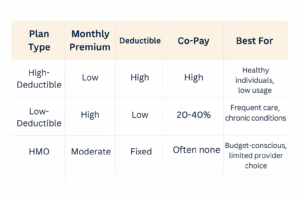

Choosing the Right Plan: What Should You Consider?

When comparing plans, think about:

- How often you use healthcare: Frequent visits? Look for low co-pays and coinsurance.

- Your budget: Can you afford a higher premium for better coverage?

- Your risk tolerance: Are you okay with paying more out-of-pocket if something unexpected happens?

Example comparison:

Final Takeaways

Understanding the difference between co-pays, deductibles, and coinsurance helps you take control of your healthcare costs. Here’s a quick recap:

- Co-pay: Fixed fee for specific services

- Deductible: Amount you pay before insurance kicks in

- Coinsurance: Percentage split after deductible is met

- Premium: Monthly cost to keep your plan active

- Out-of-pocket max: Annual cap on your spending

By knowing how these pieces fit together, you can choose a plan that works for your health needs and your wallet.

Want more clear, relatable insurance tips? Follow Insurance for Newbies for content that makes coverage make sense without the jargon.

Here’s the good news: most major insurance plans include an out-of-pocket maximum the cap on what you’ll pay in a year. Once you hit that limit, your insurance covers 100% of eligible costs for the rest of the year.

Under the Affordable Care Act, all compliant plans sold through the Health Insurance Marketplace must include an out-of-pocket maximum. Exceptions include:

- Short-term plans

- Grandfathered plans

- Limited benefit plans (e.g., accident-only or vision-only coverage)

These plans may not offer the same protections, so read the fine print.

Final Thoughts

Understanding the difference between co-pays, deductibles, and coinsurance helps you make smarter decisions about your health coverage. Whether you’re choosing a plan or explaining it to someone else, knowing how these pieces fit together can save you money and stress.

Do you want to learn more about insurance and its key terms? Follow Insurance for Newbies for clear, relatable content that makes coverage make sense. Please check out our other blogs or subscribe to our weekly digest newsletter so we can continue to post weekly blogs.